Guest post by Vaughn Stoll, SVP and Director of Acquisitions for Brown & Brown.

Significant changes in the financial environment over the past decade could potentially cut returns in half for certain private equity (PE) firms.

Fluctuations in the valuation landscape, inflation and costs of doing business have contributed to large increases in acquisition multiples and interest rates while keeping exit multiples fairly flat, resulting in much lower returns today compared to a decade ago.

You may think this drastic shift would send PE firms running for the hills, but that’s not necessarily the case. Some of the best firms are still achieving a profit — albeit a smaller one — and PE firms are largely staying in the M&A game.

What are the levers and how do they work?

2014: When everybody won

A decade ago, the PE approach benefitted from:

- Acquiring insurance agencies at low EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) multiples

- Borrowing debt at low interest rates

- Selling for substantially higher multiples

This profitable scenario typically generated high returns, which meant all stakeholders were likely to walk away with positive outcomes.

2024: Now someone may lose

Future returns are not predicated on past performance. Based on today’s variables, it’s unlikely that PE returns will continue at the pace we’ve seen in the last few years:

- Insurance agencies are being acquired at 50% higher EBITDA multiples

- Interest rates on debt have almost doubled

- Reduced arbitrage between entry and exit multiples

Imagine two start-up PE-backed agencies, both starting with $100 million in revenue, both acquiring $25 million revenue annually and both growing organically at 5%.

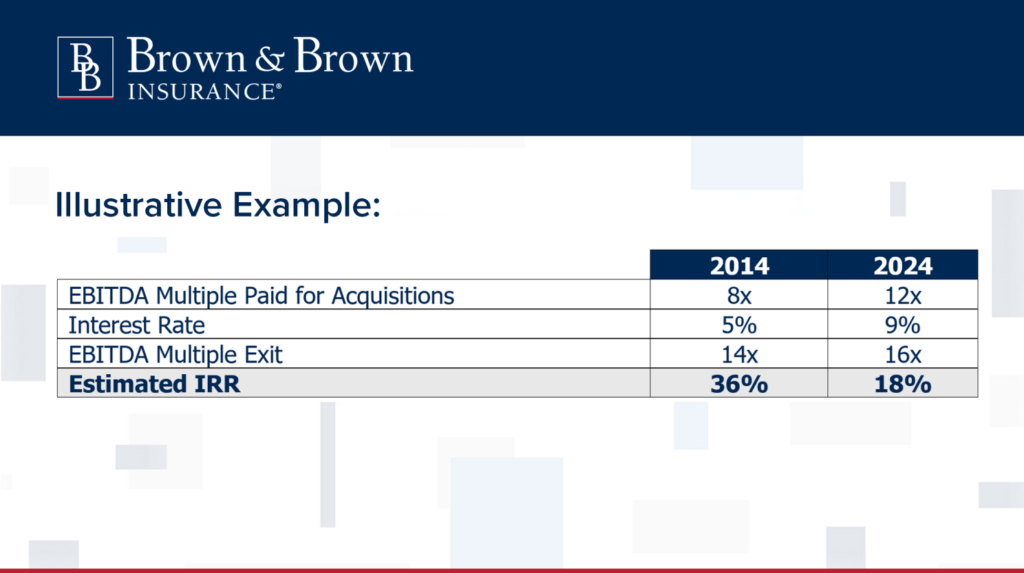

The first PE-backed agency bought agencies for 8x EBITDA. They paid 5% interest on their debt and sold with an EBITDA multiple of 14x, earning an estimated internal rate of return (IRR) of 36%.

The second PE-backed agency will pay 12x EBITDA for agencies they are acquiring. They are paying 9% interest on their debt and will sell with a projected EBITDA multiple of 16x, earning a projected IRR of just 18%. (NOTE: Although an 18% IRR doesn’t look bad, it provides a lot less cushion for unknown events. Changes in tax environment, changes in the economy, further changes in interest rates, etc., could further impact these returns.)

With an estimated 50% reduction in returns expected from an acquisition investment today compared to 10 years ago, the difference in profitability is significant. The PE model is designed to protect investor classes, and the reduction in returns will force PE firms and the agencies they acquire to find new ways to boost their returns.

Protect your business’ best interests in an acquisition

If you’re thinking about selling to a newer PE-backed firm, it’s important to understand the buyer’s exit strategy. Know what shares you will be entitled to and press for the best class of equity. Ask questions like:

- Will the firm be able to sell to another PE firm?

- If we sell to another PE firm, will I be required to roll some of my equity to the new firm?

- With 8x debt leverage, will we be able to go public?

- If we do public, how long will the stock be locked up?

- What does the initial public offering (IPO) look like for shareholders?

Look for acquisition models that not only deliver on the financial returns you deserve, but also use strategic resources and wide market reach to invest in your business’ people. Join a Forever Company.

Interested in speaking with our Mergers & Acquisitions team? Email Jimmy Curcio or acquisitionsdept@bbins.com.

This article was co-authored by Mark Prampero, Regional Director of Acquisitions, and Laban Miller, CPA, Senior Acquisitions Associate.